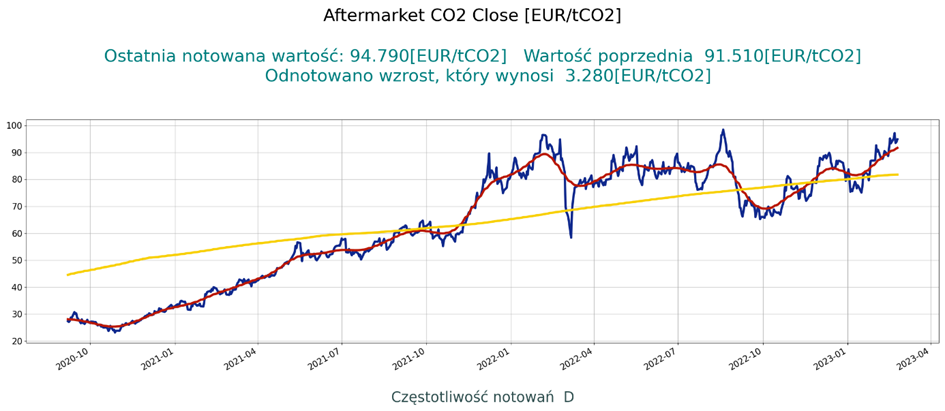

Analysis of the factors influencing prices suggests a relative balance of factors supporting the rise and fall of prices.Allowance prices in the EU ETS have long remained the highest of any emissions trading system emissions globally. This is influenced in the long term by both legal ( in force and planned), political and economic. In […]

Analysis of the factors influencing prices suggests a relative balance of factors supporting the rise and fall of prices.

Allowance prices in the EU ETS have long remained the highest of any emissions trading system emissions globally. This is influenced in the long term by both legal ( in force and planned), political and economic. In the short term, weather and the situation among various groups of CO2 rights holders have a considerable influence.

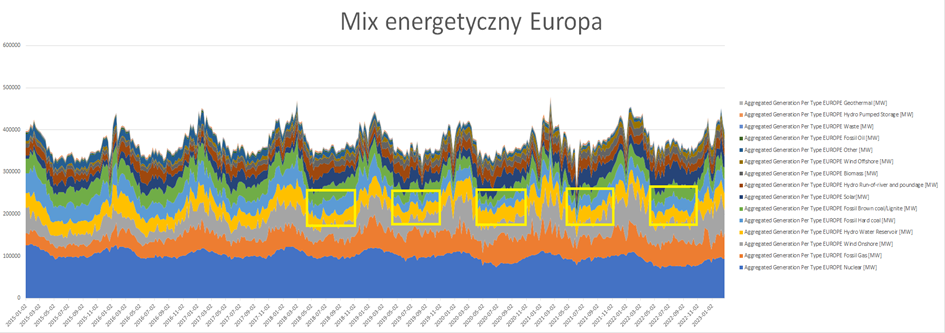

The factors mentioned above affect prices by influencing the demand and supply of allowances and shaping the energy mixes (and therefore CO2 emissions) in individual countries participating in the emissions trading system. For example in 2022, emissions from the EU electricity sector increased by 3.9% (+26 MtCO2) in 2022 compared to 2021. The reason was an increase of 7% (+28 TWh) — the use of much cheaper than gas, but more carbon-intensive coal.

The main factors shaping the price of emission allowances in Europe.

Currently, the main factors supporting price increases are:

– increase in the share of coal in the EU energy mix,

– return to a positive balance of positions taken on futures contracts by investment funds

investment funds (predominance of long positions over short positions),

– increase in the number of emission rights held by the investment fund sector,

– expectations of greater activity (production recovery) by industry in Europe due to lower

energy prices and an improved outlook for a possible recession in Europe (observed in the

several recent PMI readings).

Whereas, the main factors supporting the decline are:

– the continued decline in the number of emission rights held in the installation operators’ sector,

– the planned increase in the supply of EU ETS allowances in the coming years, due to the idea of

financing of the REPowerUE plan with revenues from the EU ETS,

– increasingly frequent periods of large shares of RES sources in the mix with increasing installed capacity of these sources (mainly wind and photovoltaic).

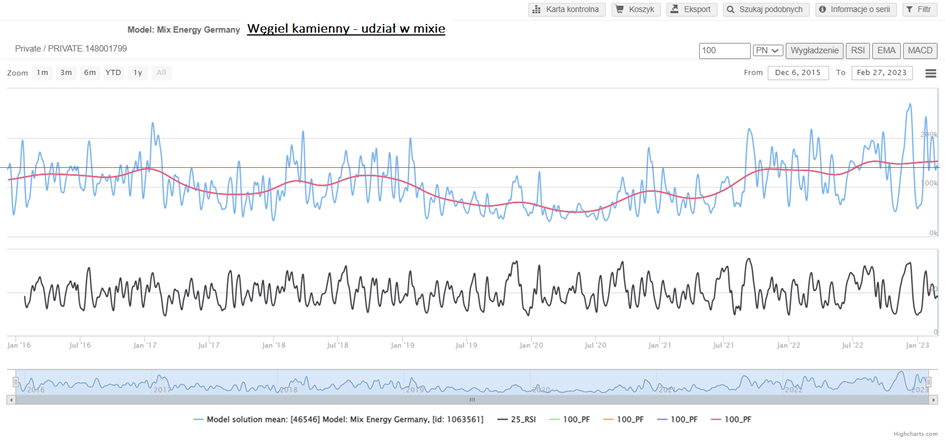

Increased use of coal for electricity generation in Europe.

Faced with an energy crisis, Europe has resumed its use of coal to generate electricity. Germany, for example, imported 44.4 million tons of coal last year, up 8 per cent from 2021. In addition, steps have been taken to bring more than a dozen coal-fired power plants back online and extend the life of several that were scheduled for closure. At the same time, the last nuclear units are being shut down. This policy is increasing the consumption of high-carbon coal, and therefore the demand for CO2 emission rights, and has been supporting price increases for several months. This situation is unlikely to change in the coming months.

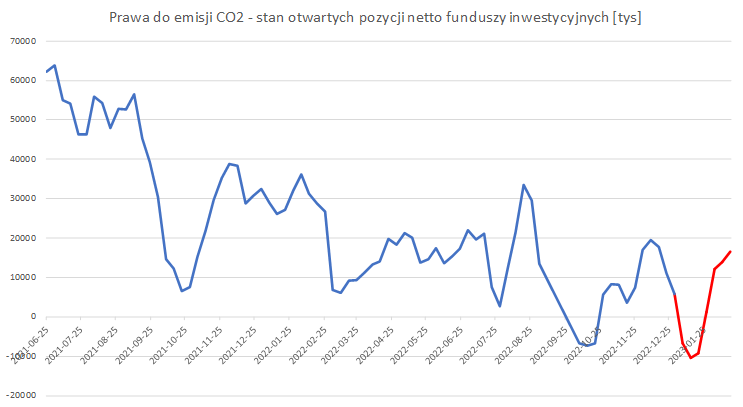

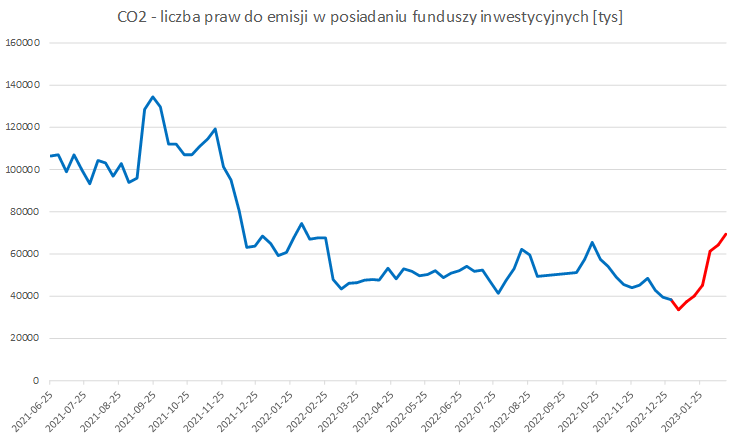

A 180-degree turnaround in the number and balance of positions taken on futures contracts.

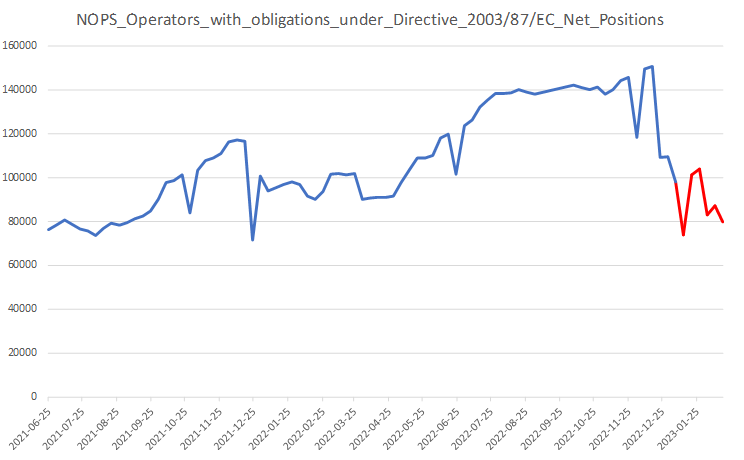

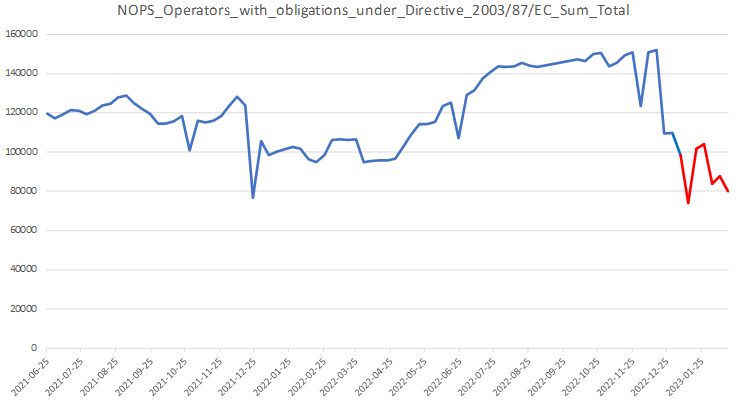

Among other things, under the influence of the information that there will be no exclusion of financial institutions from the allowances market from mid-2023, as proposed back in the autumn of 2022 (instead, there are plans for greater supervision and monitoring of the market by the European supervisory authority – ESMA), the number of emission rights held by investment funds, after several months of declines, in February again recorded increases ( from 33700 thousand to 69400 thousand). The predominance of held short positions over long positions in this group of investors, which had previously persisted for several weeks, was first levelled out and has now turned into a predominance of long positions. The state of net open positions in the mutual fund sector is now + 16525 thousand. On the other hand, the number of emission rights held by plant operators grew from the beginning of the war in Ukraine. Then at the end of the year, it fell quite sharply. This phenomenon is cyclical in this group of emission rights holders. Currently, after a temporary increase (from 74,000 thousand to 104,000 thousand), a decrease in the number of emission rights held by operators to about 80000tys is observed.

Thus, in February 2023, the influence of the investment fund sector supports the increase in the price of allowances, but the last three weeks, at the same time, is the pro-declining influence of the sector of installation operators.

Investment fund sector:

Installation operators sector:

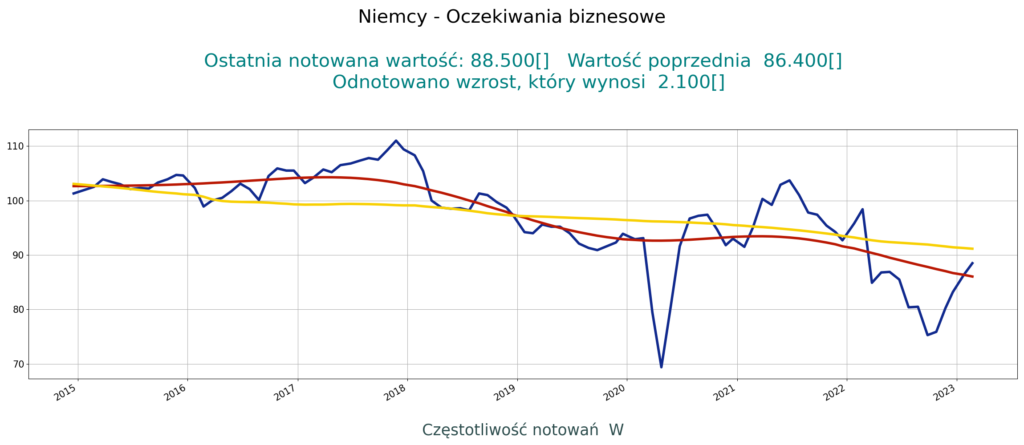

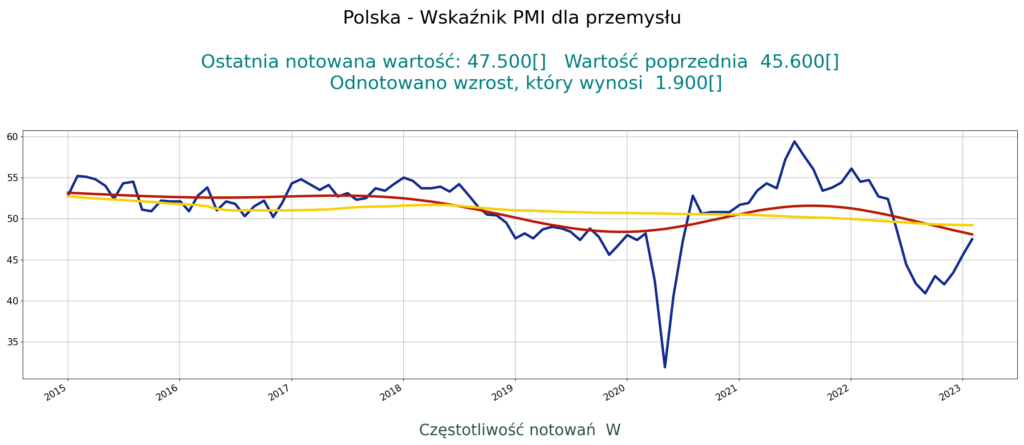

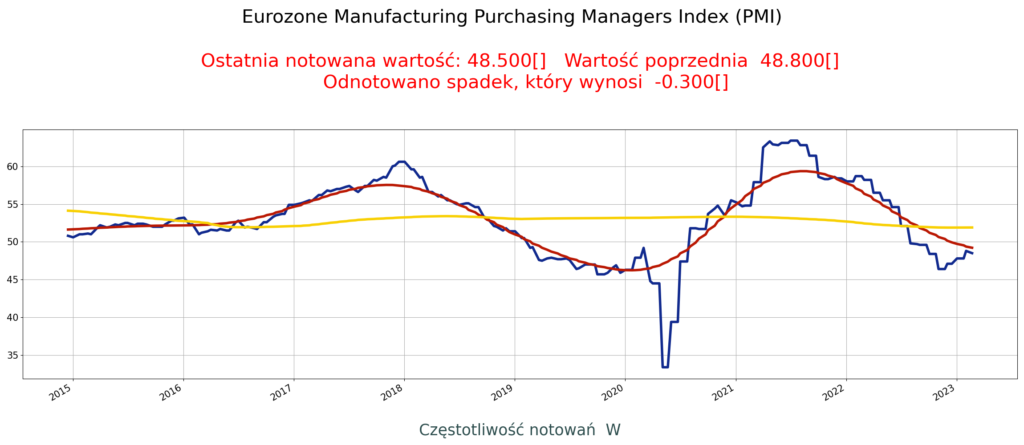

The expectation of increased activity (production recovery) by the industry in Europe.

Sustained high allowance prices should be supported by greater activity (rebuilding of production) by industry in Europe due to lower energy prices and better prospects for a possible recession in Europe. Currently, these expectations are evident in the increases in the PMIs of major economies.