An analysis of the factors influencing electricity consumption in Poland in 2023 and the first half of 2024 allows us to conclude that those that support a reduction in demand and thus reduce upward pressure on prices will prevail. These are expectations of global economic activity, projections of meteorological conditions, and projections of energy demand […]

An analysis of the factors influencing electricity consumption in Poland in 2023 and the first half of 2024 allows us to conclude that those that support a reduction in demand and thus reduce upward pressure on prices will prevail.

These are expectations of global economic activity, projections of meteorological conditions, and projections of energy demand in Poland in the coming years. They are also supported by inflation projections. A factor acting to support price increases in the period under consideration may be expectations of an increase in the price of CO2 emission rights, which in the case of Poland’s energy mix has a major impact on the cost of energy production.

The course of most of the above-mentioned factors to date, as well as projections of some of them, are shown below in graphic form. Also shown is the projection of energy prices according to the ExMetrix model, along with the factors with the greatest impact on their values.

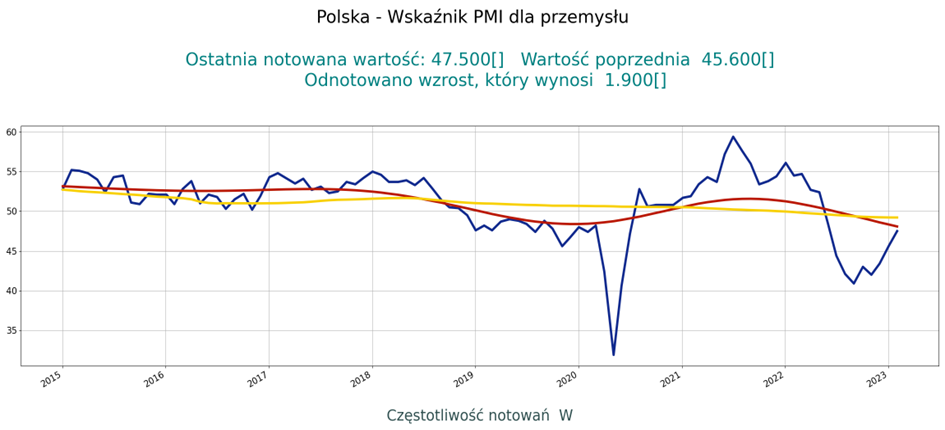

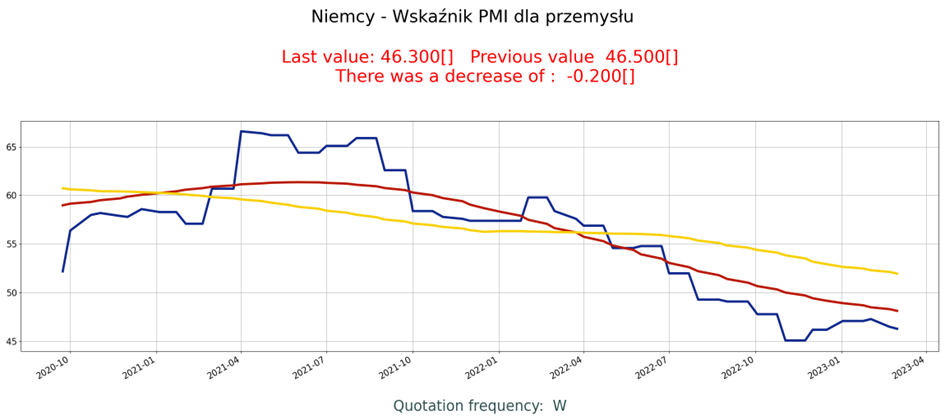

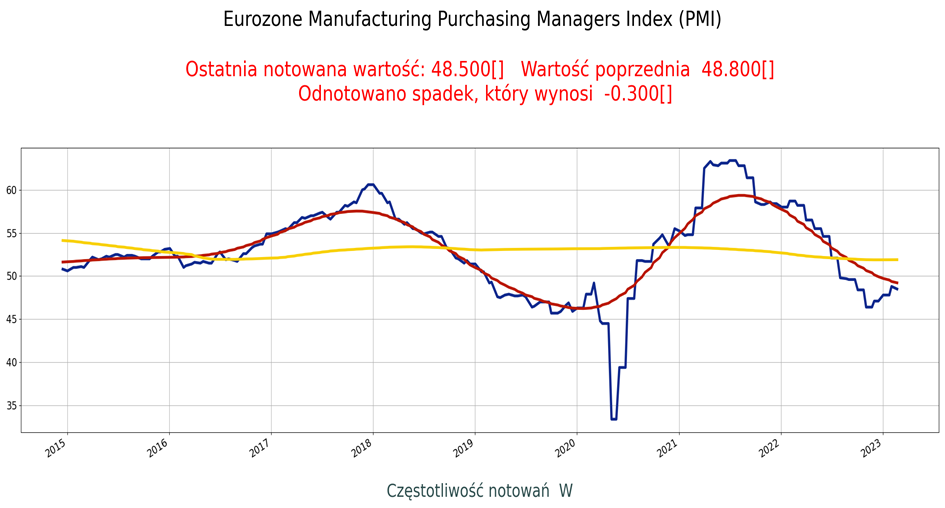

Expectations for industrial activity in Poland and Europe:

Business expectations, after several weeks of growth, stopped in Europe at below 50 points. In Germany and France, they recorded sharp declines. In general, they fit the scenario of low growth rates in 2023 in Europe, which supports a reduction in gas demand.

However, any serious revival of demand competition from China or Asia as a whole could quickly lead to price competition.

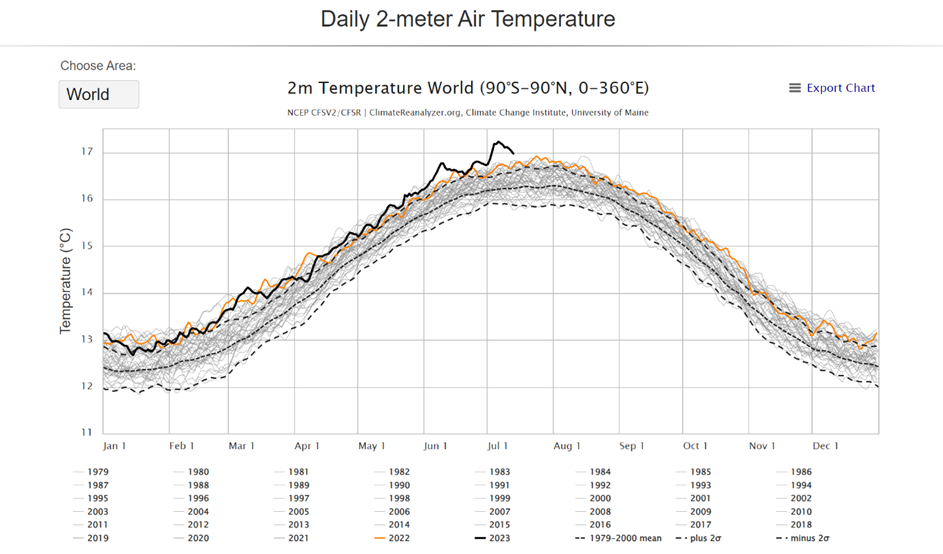

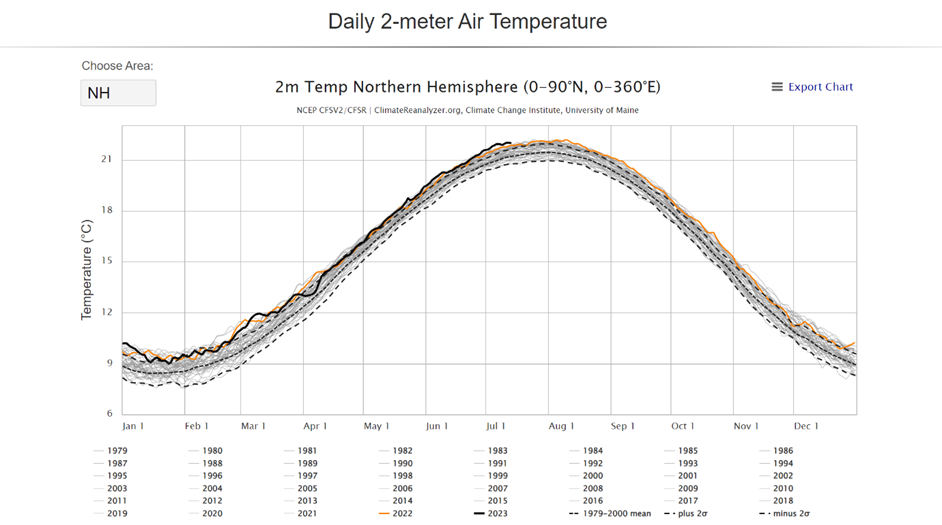

Temperatures in 2022 and 2023 higher than multi-year average:

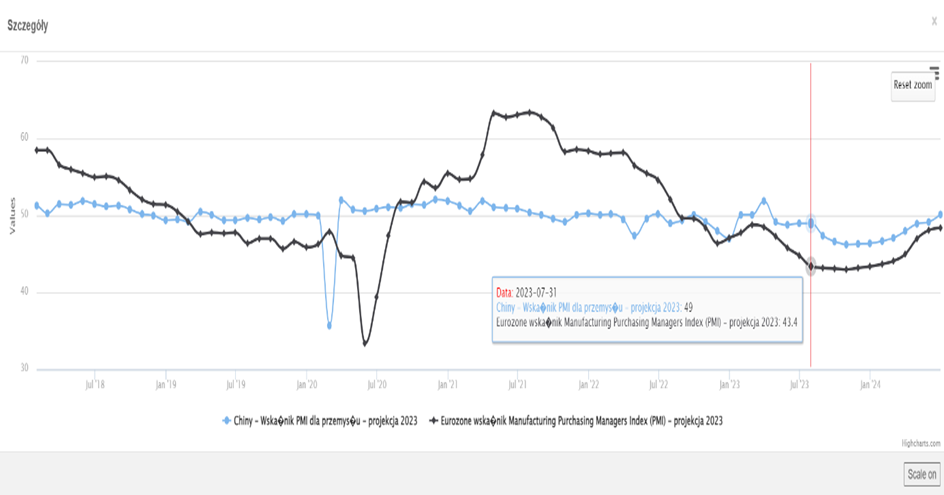

PMIs for China and the Eurozone – projections used in the energy rate model:

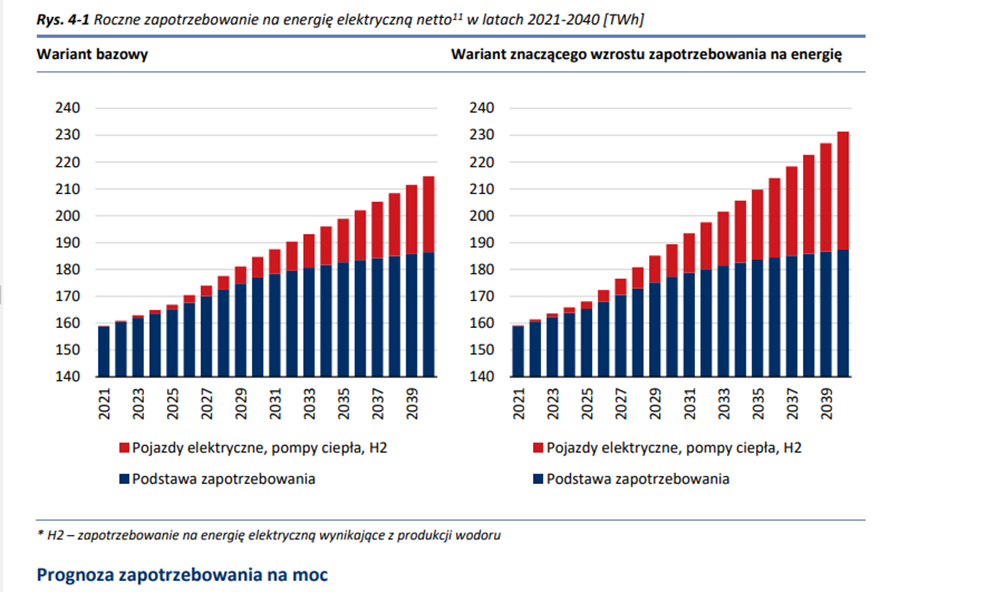

Projection (PSE) of annual electricity demand from 2021 to 2040.

The long-term forecast of net energy demand in the NPS was prepared taking into account historical trends and the forecast of final energy consumption. Macro-factors affecting the structure of energy consumption in the household, transport, industry and services sectors, changes taking place in the area of energy efficiency, forecasts of Gross Domestic Product growth in individual sectors, technological and consumer changes, as well as changes resulting from EU directives regarding Poland’s achievement of the required RES target in final energy consumption were taken into account. In addition, projected structural changes in final energy consumption were taken into account, i.e. the growth of electric vehicles, heat pumps and fuel cells, among others. Projections for electric vehicles and heat pumps were determined on the basis of publicly available data and information, as well as PSE Group’s own analyses.

The forecast was prepared in two variants, which address the adopted scenario for the development of the NPS environment.

The first is the baseline variant, while the second assumes a significant increase in energy demand. These variants are shown in the charts below. It should be noted that they do not include the demand resulting from the implementation of large industrial investments in the areas of special economic zones, which are currently in the initial conceptual stage and which are included in this plan as part of the sensitivities studied (the potential of installed consumer capacity in these zones in the next ten years exceeds 4 GW). The planned development of the transmission network addresses both variants of the demand forecast and the possible additional increase in demand as a result of the aforementioned investments.

Planned power generation corresponding to expected consumption.

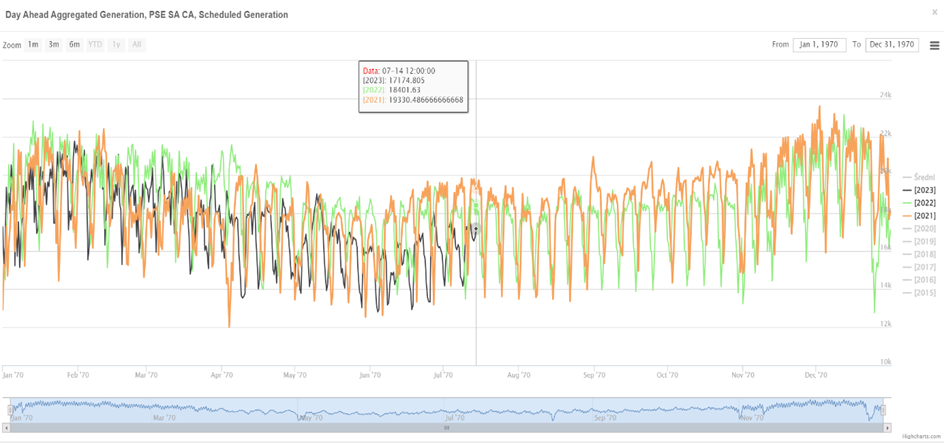

Day Ahead Aggregated Generation, PSE SA CA, Scheduled Generation [MW]:

Amount of energy produced according to scheduled power demand:

Day Ahead Aggregated Generation, PSE SA CA, Scheduled Generation [TWh]:

| 2023 | 2022 | 2021 | Period of the year |

| 80.46 | 85.78 | – | from January 01 to July 12 |

| 79.32 | 83.03 | from 01 July to 31 December | |

| 160.39 | 159.66 | All year |

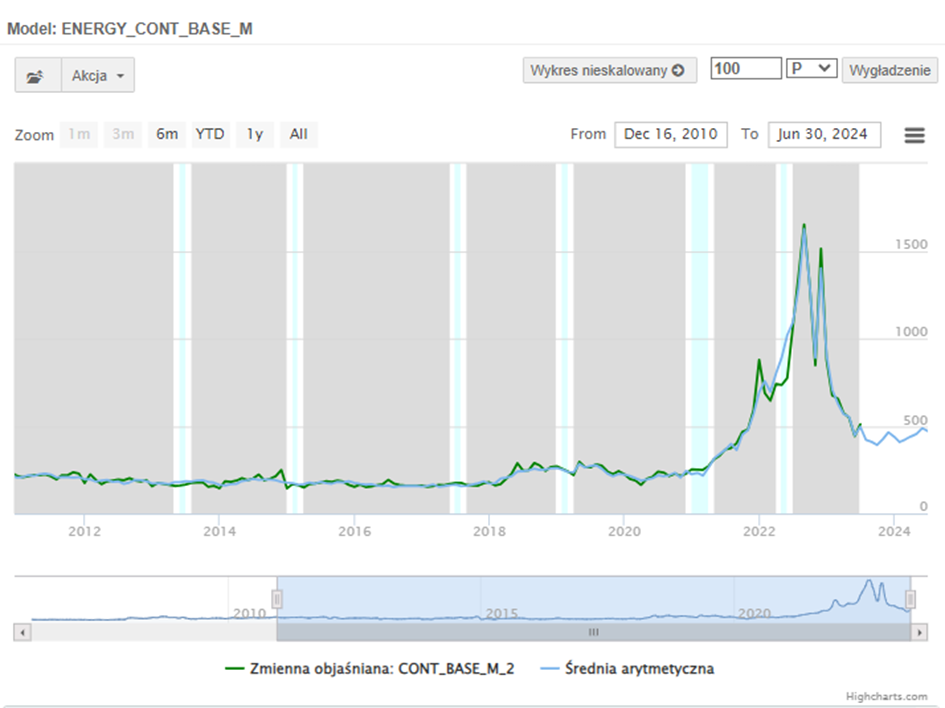

Since mid-2022, energy consumption has been clearly declining, albeit more slowly than natural gas consumption over the same period. In 2023, judging from calculations so far, energy consumption may be lower than in 2022 by about7%. We have made this assumption for the energy price forecasting model.

Energy generation and demand in Europe.

The outlook for French nuclear power generation in 2023 is more positive than in 2022. reactors shut down due to corrosion problems are returning to operation. however, complications from adverse dry and warm weather leading to outages are still likely in 2023.

Nonetheless, availability remains well below historical norms for the start of the year, while the Grand Carénage reactor expansion program will continue to limit production, and the Flamanville start-up will not take place in 2023. If the midpoint of EDF’s current estimated production (315TWh) were achieved, this would represent an increase of 38TWh over 2022. In addition, Slovakia is expected to see 4TWh of additional supply from the commissioning of Mochovce Unit 3.

However, these gains will be offset by declines in Belgium and Germany. The Belgian decline is expected to be around -20 TWh from the closure of Tihange 2 at the end of January, following the closure of Doel 3 in September 2022. A similar decline (-22 TWh) occurred in Germany, where the last nuclear units were closed in April.

Growth in solar and wind power is expected to increase by 82 TWh from last year (up from 59 TWh in 2022), although production depends on weather. Growth will be driven by a combination of increasing solar and offshore wind capacity, while the addition of onshore wind is expected to remain at 2022 levels.

It is difficult to predict hydropower performance for 2023, although it is worth noting that southern European countries entered the new year with stocks at levels close to the average of the past five years, following a rebound late in the year.

Energy demand is likely to remain subdued in 2023, as the high price environment continues to drive changes in industrial, commercial and residential consumer behavior. Our analysis shows that winter demand in 10 EU countries (accounting for ~80% of the bloc’s demand) has declined by 7% since the beginning of November 2022 compared to the average of the previous five years. This is just below the 10% voluntary target agreed to by member states in October. However, as mentioned earlier, it is difficult to determine the impact of temperatures on the decline in demand.

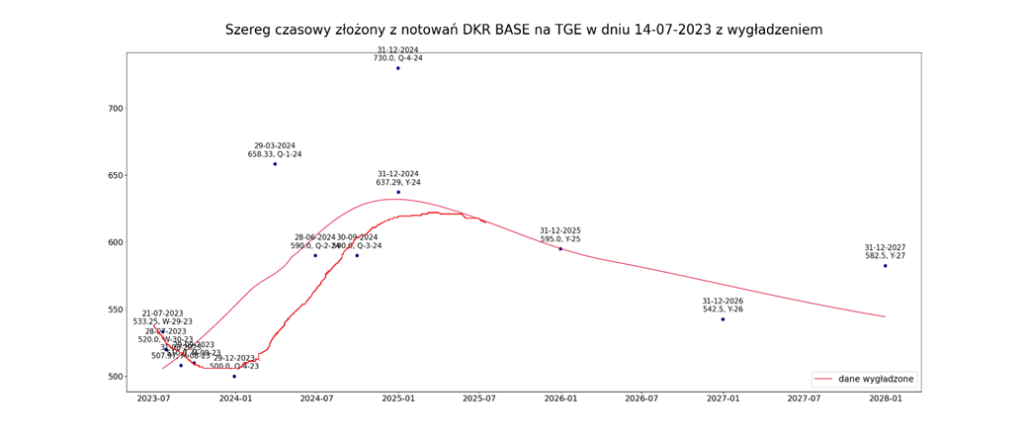

Ex Metrix Model

We expect a decline in energy prices until the end of September , and then an increase, which will be about 15%. In total, the model implies a decline in energy prices by the end of the year of about 10%, which agrees quite well with current expectations of market participants.

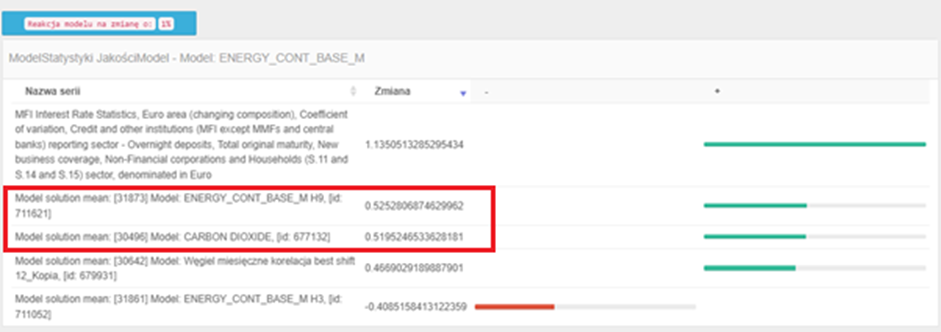

MFI (Monetary Financial Institutions) interest rate statistics, Eurozone (changing composition), volatility factor, credit and other institutions reporting sector (MFIs excluding MMFs and central banks) – deposits per day, total primary period, new business coverage, non-financial corporations and households sector (S.11 and S.14 and S.15), denominated in euros.