The Polish coal market is increasingly tied to the global market. One of the reasons for this is the quoting of the proposed energy price in the balancing market based on generation costs compulsorily calculated based on the mix of ARA coal and PSCMI 1/T middlings. Mandatory inclusion of PSCMI 1/T middlings began in 2022 […]

The Polish coal market is increasingly tied to the global market. One of the reasons for this is the quoting of the proposed energy price in the balancing market based on generation costs compulsorily calculated based on the mix of ARA coal and PSCMI 1/T middlings. Mandatory inclusion of PSCMI 1/T middlings began in 2022 , with PSCMI 1/T prices significantly lower than ARA coal prices at the time, and was intended to make Polish generators’ generation costs more realistic.

Following the renegotiation of contracts for the purchase of coal by Polish power producers from PGG, there was a sharp increase in the price of PSCMI 1/T. At the same time, prices on the world market fell sharply. At the end of March 2023, the PSCMI 1/T price was 164.3 [USD/T], while the ARA coal price was 142.15[USD/T] (annual contract). PSCMI 1/T price readings for April have not yet been published, but the price of ARA coal fell between March 31, 2023 and May 15, 2023 to 109.55 [USD/T]. Is the PSCMI 1/T likely to follow in the footsteps of ARA coal, and possibly when?

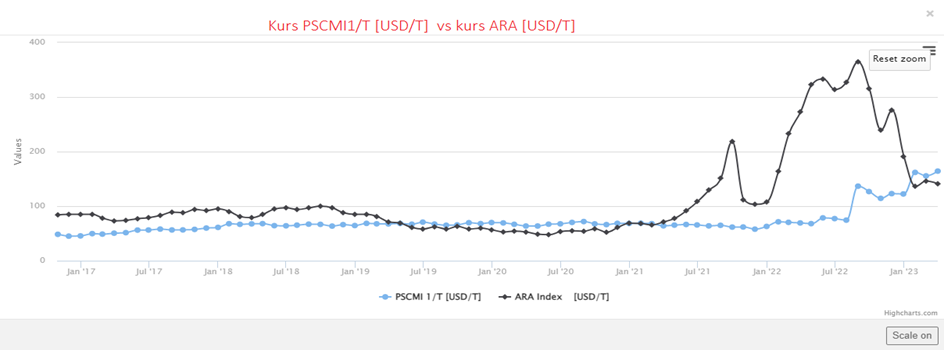

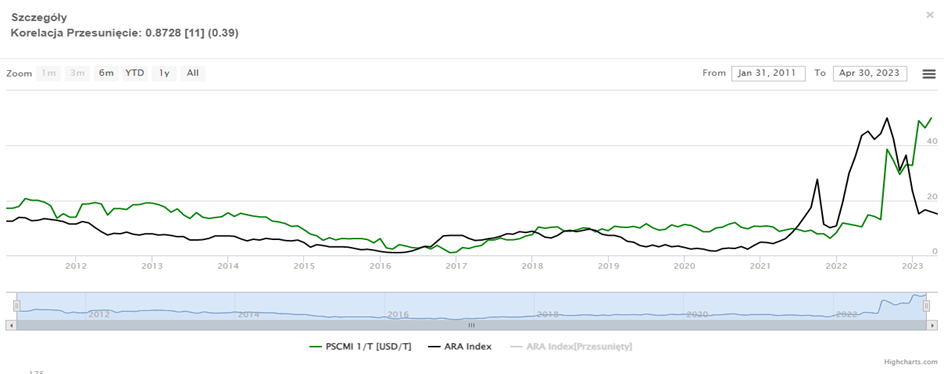

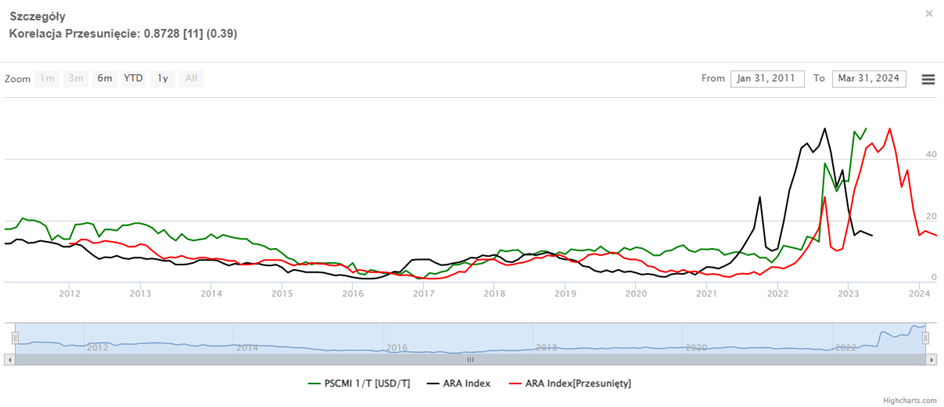

Below is the course of the two bourses on the same scale. It turns out that the situation in the ARA coal market has been about 11 months ahead of what is happening in the domestic market for several years. In addition, it turned out that after taking this advance into account, the correlation coefficient of the two variables from 2011 to 2023 was high at 0.8728. Without taking the advance into account, the correlation was „only” 0.48.

Thus, analyzing the historical course of both rates and taking into account the 11-month advance of the global market relative to the domestic market, a more pronounced decline in the PSCMI 1/T rate is expected around October 2023 (red line in the chart below).

This scenario is further supported by the result of testing the cointegration (long-term relationship) of the two variables.

Cointegration is a property of time series used in econometrics, which occurs if two time series are not stationary, but their linear combination is stationary. In simpler terms, when the series are cointegrated, it can be assumed that there is a long-run relationship between them.

One method for testing cointegration is the Johansen method, which consists of two tests: the trace test and the largest eigenvalue test.

After applying the Johansen method to the odds of PSCMI 1/T coal and ARA coal, it turned out that the results of the trace test and the largest eigenvalue test indicate the existence of a single cointegrating vector. Thus, a long-term relationship between these quantities can be expected.

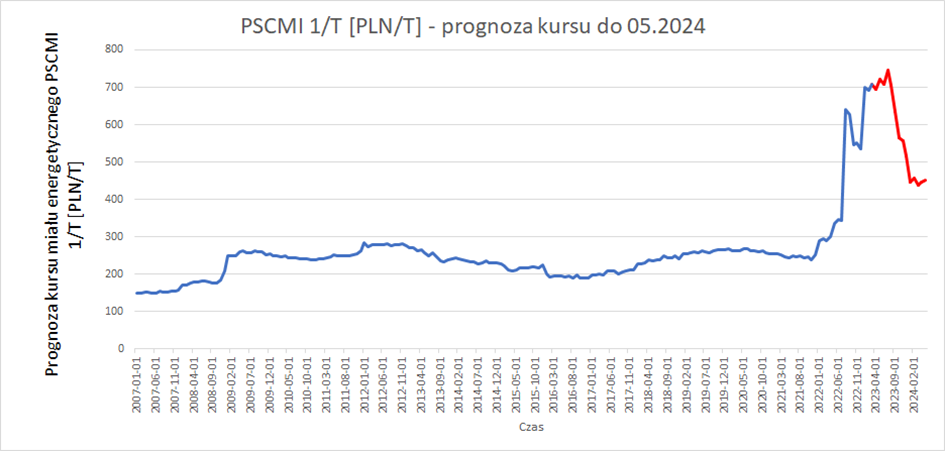

After taking into account the relationship between the ARA exchange rate and PSCMI 1/T, as well as information on expectations about the economic situation in Poland, a model was built to forecast the course of the PSCMI 1/T exchange rate for the next 12 months. The model was optimized using machine learning. The result is shown in the chart below: