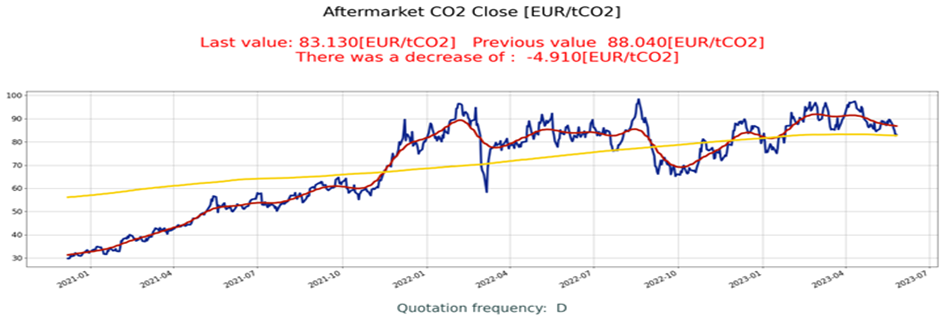

It cannot be ruled out that, in the long term, market participants expect CO2 volumes to fall due to the expected economic slowdown or even recession in the EU. In addition, improvements in energy efficiency and greater use of RES sources for energy production support price declines. The fact that the EU Council adopted the […]

It cannot be ruled out that, in the long term, market participants expect CO2 volumes to fall due to the expected economic slowdown or even recession in the EU. In addition, improvements in energy efficiency and greater use of RES sources for energy production support price declines. The fact that the EU Council adopted the reform of the EU system may also have acted similarly.

It is apparent that the course has struggled to overcome previous peaks in 2022:

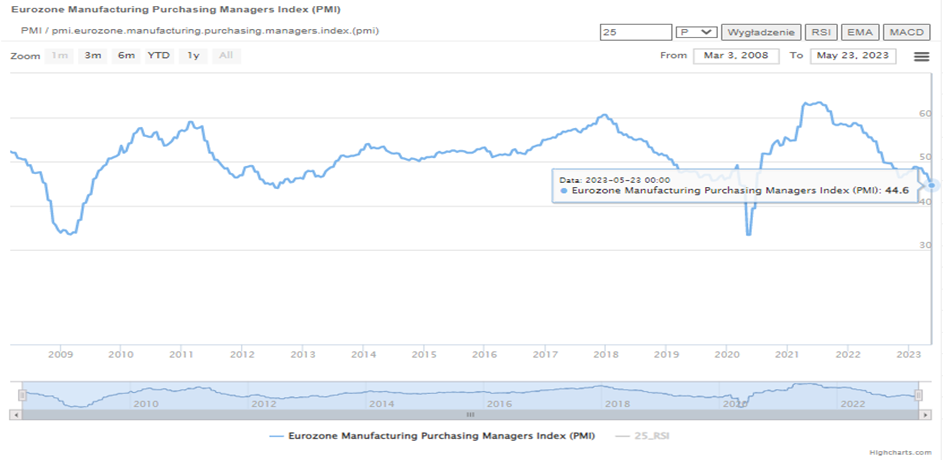

Weak economic situation in Europe.

Measurements of the PMI index for European industry indicate a deepening crisis. In May (May 24, 2023), the index calculated for the eurozone fell to 44.6 points from 45.8 points . with the equilibrium level at 50 points. Anything below that means expectations of declines. This is the worst data since June 2020, the first wave of the pandemic.

For Europe’s largest economy, Germany, the index fell to 42.9 points from 44.5 in April. Germany’s manufacturing sector once again slightly increased output in April. At the same time, signs of weak demand are noticeable. This is most evident in the PMI sub-index for new orders, which again signals declines, including declines in orders from abroad. Shorter recorded delivery times do not change the fact that demand is weakening.

Of course, these circumstances support the decline in the allowance rate.

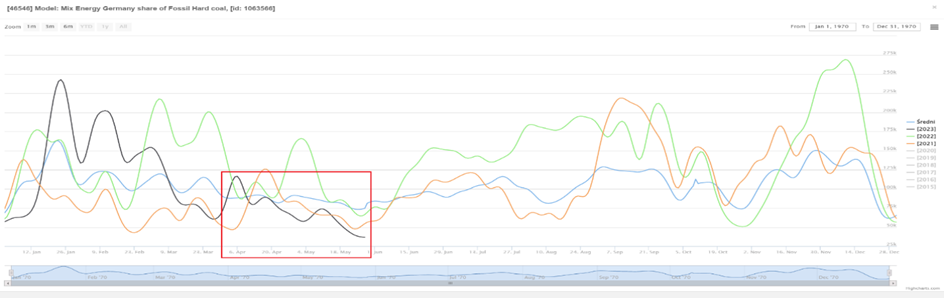

Falling share of coal in the energy mix in Germany.

In addition to macroeconomic problems, the decline in the price of allowances over the next few months will be supported by the already apparent low share of energy generated from coal in the EU’s largest economy, Germany. This is due to favorable weather and record energy production from RES this year.

This situation is likely to continue until the beginning of the next winter season. Then the fact that in April 2023 Germany said a definitive farewell to nuclear power, forcing the country to replace nuclear units with coal ones, may make itself known. This was already evident in the winter of 2022/2023, when the share of energy produced from coal far exceeded the multi-year average.

Germany – currently the share of coal in the mix below the average of the last 9 years (3.6%), and in the completed winter – clearly above (max. almost 25%):

In the next winter season, the share of coal in the mix is likely to increase significantly from the level observed today.

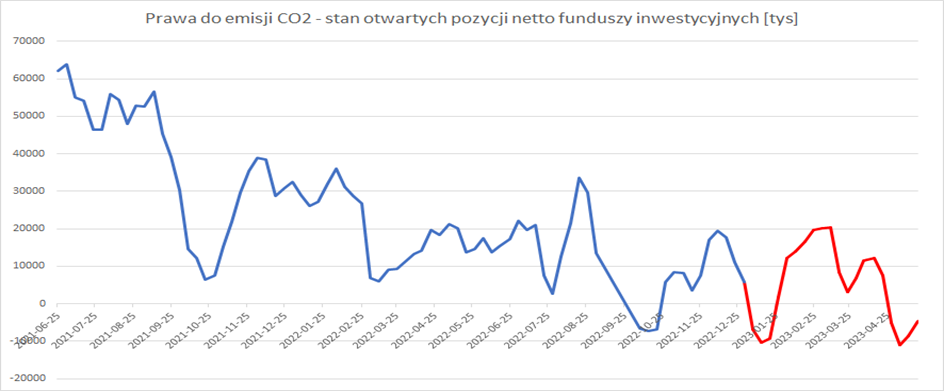

The balance of open positions on CO2 emission rights futures contracts in the mutual fund sector is currently negative.

The balance has been in a downward trend for a long time for various reasons, including expected regulatory changes. It is currently negative, meaning that short positions prevail, so investors are setting themselves up for declines:

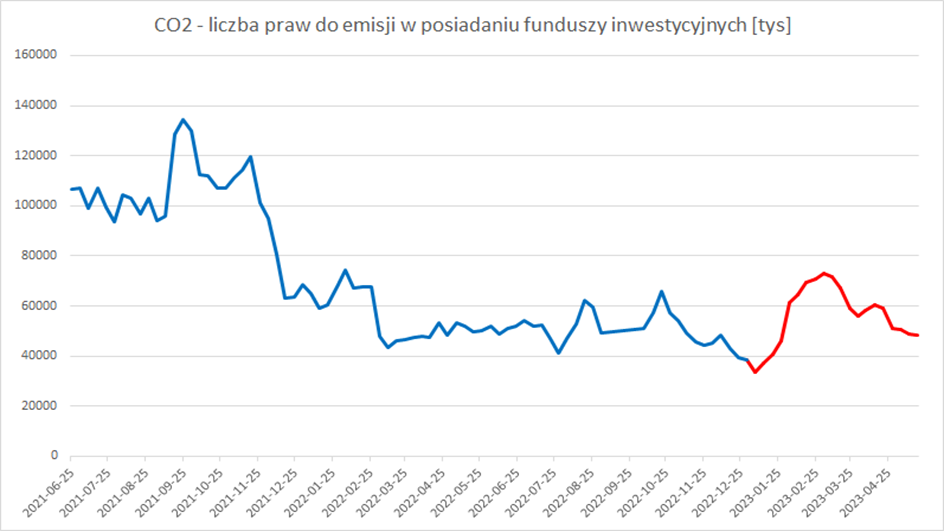

In addition, the number of emission rights held by the funds is now comparable to the number of rights resulting from positions opened by installation operators in the secondary market:

It follows that currently the dominant influence on the volatility of the price of emission rights again belongs to investment funds, which naturally also increases the risk of speculative activities in this market.

Based on the rationale cited, a model was constructed to forecast the price of emission rights over a 12-month horizon:

The forecast suggests a fluctuating rate with a slight downward trend over the next nine months, with an upward trend in the spring of 2024. Support for the increases may come during the winter season from the increased share of coal-fired power generation in Europe.

The model was estimated using machine learning.

The beginning of a more stable increase in allowance prices is expected in the following months of 2024 and beyond, as a result of an improvement in the macro situation in Europe and the US and a possible recovery in China (delayed for now by the weak economy).

In line with the above economic expectations, average allowance prices in 2025 should be above €100. The increase in allowance prices should be supported by greater activity (production recovery) by industry in Europe due to expected lower energy prices and better prospects for a possible recession in Europe.

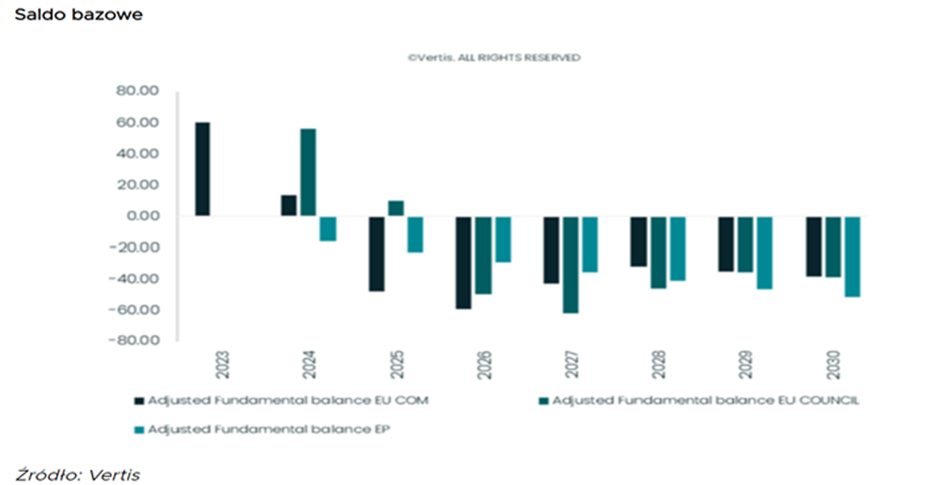

The balance analysis (supply-demand for allowances) is supported by the supply assumption presented by the EC, according to which the volume of allowances will be increased by 79 million more in 2023 (Council of Europe: 75 million in 2024). The European Parliament, on the other hand, refers to a value of 112 million in 2024. On the demand side, based on MRV data, a value of 90 million EUAs is expected if the EC and EU Council’s assumptions work out, or 129 million if the Parliament’s proposal is supported, due to the difference in allowance surrenders for non-EU voyages.

In general, from 2025 the balance may be negative, which will favor price increases: