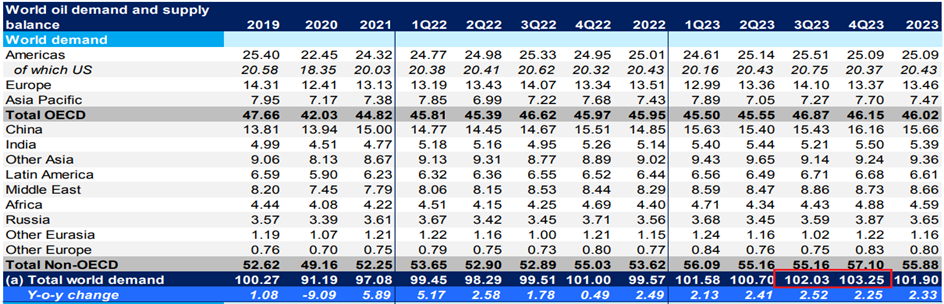

Both the International Energy Agency and OPEC+ expect a further increase in global oil demand in the second half of 2023, potentially lifting oil prices. The recovery expected in a few months is expected to contribute to this. At present, however, supply is not aligned with the record high level of production in the U.S. […]

Both the International Energy Agency and OPEC+ expect a further increase in global oil demand in the second half of 2023, potentially lifting oil prices. The recovery expected in a few months is expected to contribute to this.

At present, however, supply is not aligned with the record high level of production in the U.S. , nor Russia’s higher-than-expected exports, nor the generally weak economic situation in both China and the U.S., and especially in Europe. In general, according to many analysts, supply is currently too high.

Expected oil demand growth in Q3 and Q4 2023:

Source: OPEC+

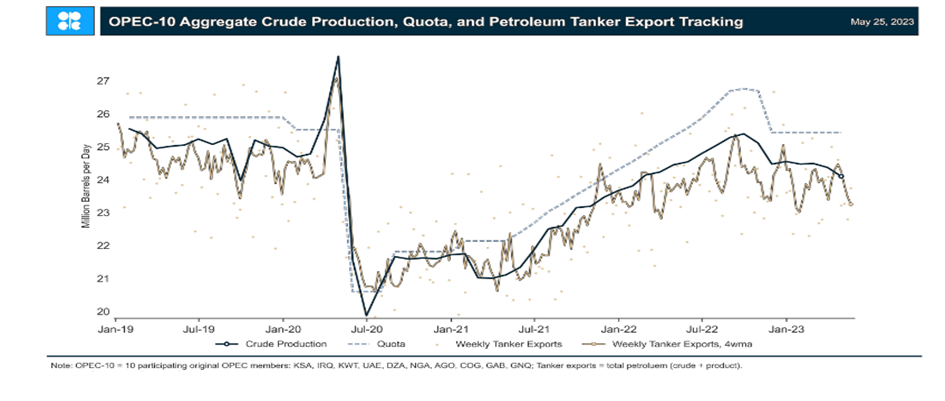

Expected output cuts by OPEC+ members.

A two-day OPEC meeting began on Saturday, 03/06/2023, which could result in a cut of 1 million bpd on top of existing cuts of 2 million bpd and voluntary cuts of 1.6 million bpd announced in a surprise move in April that went into effect in May. If this scenario is approved, the total size of the reduction will rise to 4.66 million bpd, or about 4.5% of global demand.

Production to date, tanker exports and production levels corresponding to the current OPEC+ cuts:

Source: OPEC+, EIA, Commodity Context

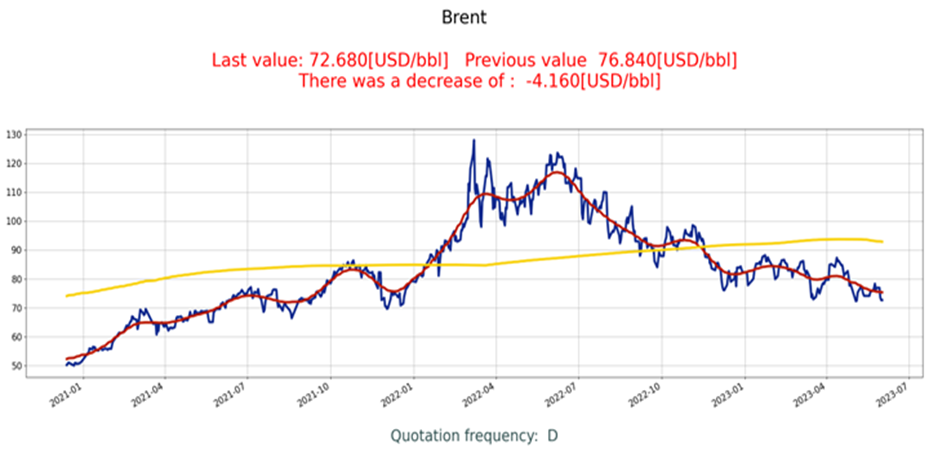

Brent crude oil price:

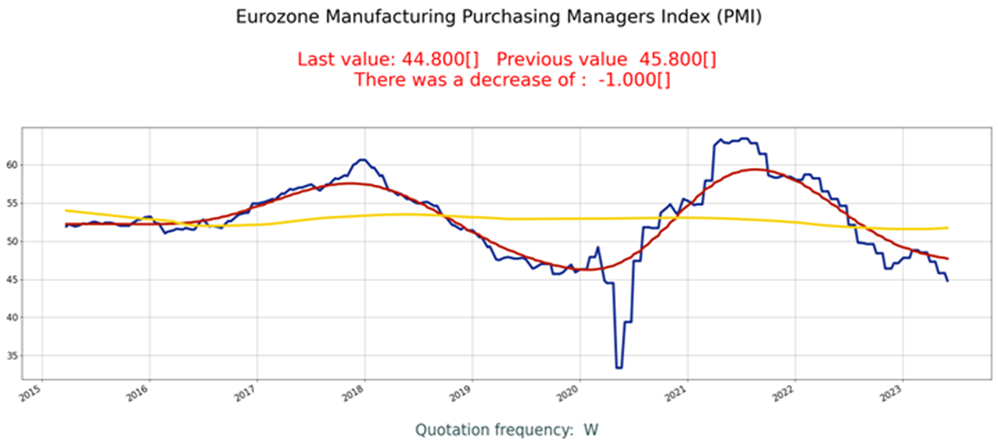

Weak economic situation.

Measurements of the PMI index for European industry indicate a deepening crisis. In May (May 24, 2023), the index calculated for the eurozone fell to 44.6 points from 45.8 points . with the equilibrium level at 50 points. Anything below that means expectations of declines. This is the worst data since June 2020, the first wave of the pandemic.

In China, after a temporary uptick driven by better GDP readings, the PMI index fell for the third consecutive time and is below the 50-point level:

The US manufacturing PMI also failed to stay above 50 points:

A negative balance of open positions of large investors.

The risk from positioning on BRENT crude oil is clearly biased toward rising prices, especially if the net worth remains low and with a large number of large gross short positions. Large investors maintain sizable short positions, so there is a risk of closing these positions if prices begin to rise , for example, after news of further planned cuts, signals of an upturn, or an actual decline in production. This means that large speculators will be forced to buy contracts to meet their commitments. Such a situation can further raise prices. This is the so-called „short squeeze” effect. In general, the probability of a sharp rise in prices increases if speculators begin to close their short positions en masse.

A large number of large gross short positions – balance MINUS ( black dot chart at the bottom of the image):

Data: CFTC, compilation – ExMetrix

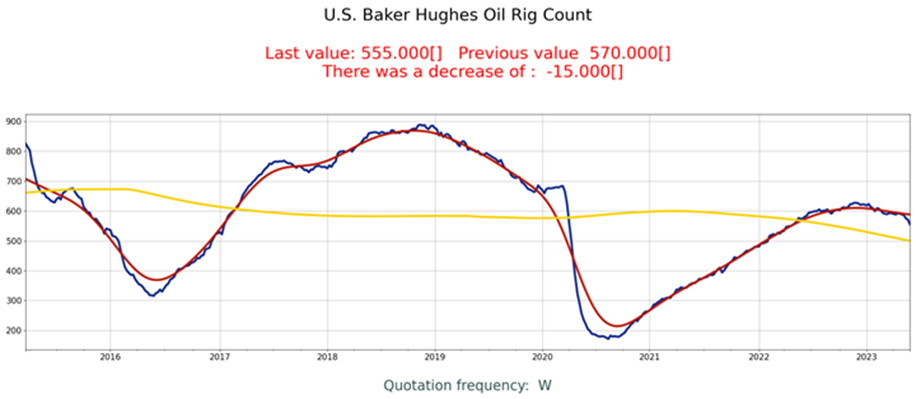

U.S. production at risk of decline.

U.S. oil and gas producers are cutting back on drilling activity for the first time since the initial phase of the COVID-19 pandemic – and this could have a dramatic impact on global balance sheets with strong demand growth forecast for the second half of 2023. Every rig shut down means slower production growth in the US, and this is taking place in the face of a significantly reduced number of available but unfinished wells.

Given the lag of several months in the cycles from price to rig and to product, it is reasonable to expect a further slowdown in oil activity to continue for the rest of the year, long after prices have risen again to sufficiently supportive production levels.

This is particularly worrisome given the critical importance of US production growth to global market balances. Both EIA and OPEC are still projecting total U.S. production growth of nearly 1 MMbpd in 2023.

It will be extremely difficult to achieve these optimistic estimates with fewer and fewer wells open.

For now, we are at best in the very early stages of a slowdown. But we are certainly not in a good position, given several factors. First, the efficiency gains that still exist mean that every single rig lost is more important to production growth today than in the past.

Second, the U.S. has significantly depleted its once-accumulated inventory of wells not yet completed (DUCs).

Finally, a lag of several months in the price-driller-product cycles means that we have yet to really feel the impact of the price declines of early 2023. Lower prices are expected to continue to put downward pressure on the number of drillers.

Number of open oil wells in the US:

Individual production basins in the U.S. and shale oil production:

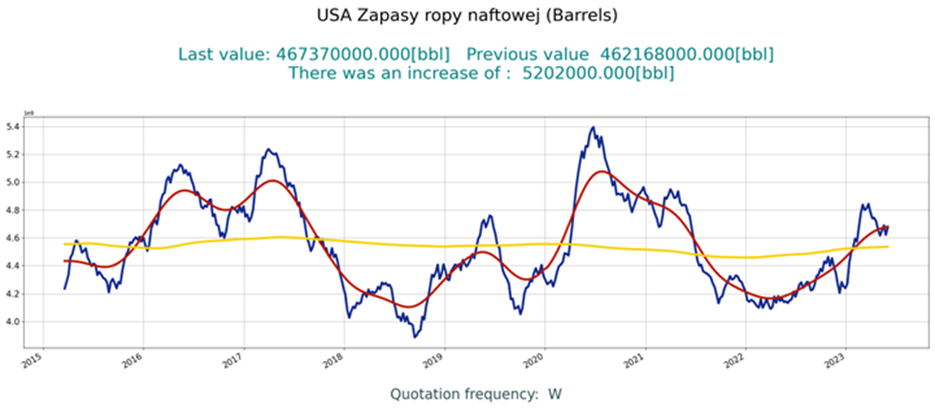

Commercial oil stocks in the US, Singapore and ARA region higher than last year.

In March, Singapore’s crude oil stocks rose month-on-month by 2.9 million barrels, reaching 48.0 million barrels. This is 6.5 million barrels, or 15.7%, higher than in the same month in 2022, and 0.4 million barrels, or 0.9%, higher than the average for the past five years.

Total product stocks in ARA rose by 0.7 million barrels month-on-month in March. At 46.5 million barrels, they were 7.3 million barrels, or 18.6%, higher than in the same month in 2022, and 2.9 million barrels, or 6.7%, higher than the latest five-year average.